Credit Rating in Bangladesh

by Admin-KCBD · Published · Updated

Credit Rating in Bangladesh: The Definitive Guide to Scores, Agencies, Scales, and Strategic Implications

The Silent Gatekeeper of Bangladesh's Financial System

A mid-sized garment manufacturer in Gazipur applies for a ৳50 crore term loan from a leading private commercial bank. The financial statements look adequate. The collateral appears sufficient. The business is operational and profitable. Yet the loan is declined — or offered at a punishingly high interest rate that renders the financing economically unviable.

The reason, in most cases, comes down to a single analytical output that the business owner may not fully understand: the credit rating.

In Bangladesh’s evolving financial architecture, credit rating functions as the invisible gatekeeper between capital seekers and capital providers. A strong rating unlocks financing at competitive terms. A weak rating — or the complete absence of one — signals elevated risk to lenders and investors, triggering either rejection or prohibitive pricing. The asymmetry is significant: businesses and institutions that understand and actively manage their credit profile gain meaningful competitive advantages in accessing the Bangladesh capital market and banking sector.

This guide provides a complete, clinical examination of credit rating in Bangladesh — the agencies, the scales, the grades, the process, the regulatory mandates, and the strategic implications for every stakeholder in Bangladesh’s financial ecosystem.

What Is Credit Rating? Foundational Definitions

Defining Credit Rating in the Bangladesh Context

A credit rating is a formal, independent assessment of the creditworthiness of an entity — a company, financial institution, government body, or specific debt instrument — expressed as a standardized alphanumeric grade on a defined rating scale. The rating communicates the probability that the rated entity will meet its financial obligations in full and on time.

In the context of credit rating in Bangladesh, the assessment evaluates:

- Capacity to repay — Does the entity generate sufficient cash flow to service debt obligations?

- Willingness to repay — Does management demonstrate a historical commitment to honoring financial obligations?

- Financial structure — Is the balance sheet appropriately leveraged relative to earnings and asset base?

- Industry and operating environment — Do sector dynamics and macroeconomic conditions support or constrain the entity’s financial performance?

- Governance and management quality — Are oversight structures, internal controls, and strategic decision-making sufficiently robust?

A credit rating is not a recommendation to buy, sell, or hold a security. It is specifically a risk opinion regarding default probability — a standardized signal designed to reduce information asymmetry between issuers and investors or lenders.

Credit Rating vs. Credit Score in Bangladesh

A frequent source of confusion in the Bangladesh financial market is the distinction between a credit rating and a credit score:

| Dimension | Credit Rating | Credit Score in Bangladesh |

|---|---|---|

| Subject | Corporates, banks, financial institutions, instruments | Individual consumers and small borrowers |

| Expressed As | Alphanumeric grade (AAA, AA, A, BBB, etc.) | Numerical score (typically 300–900 range) |

| Produced By | Licensed credit rating agencies | Credit Information Bureau (CIB) of Bangladesh Bank |

| Primary Users | Capital market investors, institutional lenders, regulators | Retail banks, MFIs, consumer lenders |

| Regulatory Mandate | BSEC, Bangladesh Bank circulars | Bangladesh Bank CIB framework |

| Review Frequency | Annual (or triggered by material events) | Updated with each credit facility report |

The Credit Information Bureau (CIB) maintained by Bangladesh Bank is the primary institutional repository for individual and SME borrower credit data in Bangladesh. While it performs a credit scoring function for retail lending decisions, it is structurally distinct from the formal credit rating system in Bangladesh administered by licensed rating agencies.

Credit Rating Agencies in Bangladesh: The Institutional Landscape

Licensed Credit Rating Companies in Bangladesh

The Bangladesh Securities and Exchange Commission (BSEC) licenses and supervises credit rating agencies operating in Bangladesh under the Credit Rating Companies Rules, 1996. As of the most recent regulatory registry, the following are the principal credit rating agencies in Bangladesh:

| Agency | Abbreviation | International Affiliation |

|---|---|---|

| Credit Rating Agency of Bangladesh Limited | CRAB | Affiliated with international rating methodology frameworks |

| Credit Rating Information and Services Limited | CRISL | Technical collaboration with Japan Credit Rating Agency (JCR) |

| Emerging Credit Rating Limited | ECRL | Domestic rating agency |

| National Credit Ratings Limited | NCR | Domestic rating agency |

| WASO Credit Rating Company (BD) Limited | WASO | Domestic rating agency |

| Alpha Credit Rating Limited | Alpha | Domestic rating agency |

Each licensed credit rating company in Bangladesh must maintain methodological consistency, analytical independence, and compliance with BSEC’s regulatory directives. Rating analysts are prohibited from having financial interests in the entities they rate — a structural safeguard against conflict of interest.

You can always find the latest listed credit rating agency by BSEC here: BSEC List of Credit Rating Agencies

Regulatory Oversight of Rating Agencies

The governance of credit rating agencies in Bangladesh operates under a layered regulatory framework:

- BSEC (Bangladesh Securities and Exchange Commission) — Primary licensing and oversight authority for rating agencies; mandates rating requirements for capital market issuances

- Bangladesh Bank — Requires credit ratings for financial institutions seeking certain regulatory classifications and for bond/sukuk issuances by banks

- Credit Rating Companies Rules, 1996 — The foundational legal framework governing agency operations, methodology standards, conflict of interest provisions, and disclosure requirements

- IOSCO Code of Conduct Fundamentals — International best practice framework that Bangladesh’s rating agencies are progressively aligning with

The Credit Rating Scale in Bangladesh: Understanding the Grading Architecture

Long-Term Credit Rating Scale

The credit rating scale in Bangladesh for long-term obligations follows an alphanumeric grading system broadly aligned with international rating conventions. The following represents the standard long-term scale used by principal Bangladeshi rating agencies:

| Grade | Category | Interpretation |

|---|---|---|

| AAA | Highest Safety | Exceptional capacity to meet financial commitments; lowest default risk |

| AA+, AA, AA- | High Safety | Very strong capacity; marginally more susceptible than AAA to adverse conditions |

| A+, A, A- | Adequate Safety | Strong capacity; somewhat more susceptible to adverse economic conditions |

| BBB+, BBB, BBB- | Moderate Safety | Adequate capacity; adverse conditions more likely to impair capacity |

| BB+, BB, BB- | Moderate Risk | Speculative elements; faces ongoing uncertainties |

| B+, B, B- | High Risk | Currently meets obligations; adverse conditions would likely impair capacity |

| CCC | Very High Risk | Currently vulnerable; dependent on favorable conditions for continued servicing |

| CC | Extremely High Risk | Highly vulnerable; near default |

| C | Imminent Default | Default imminent; recovery expected |

| D | Default | Actual failure to meet financial obligations |

Grades from AAA through BBB- are classified as Investment Grade — indicating adequate to exceptional creditworthiness. Grades from BB+ and below are classified as Speculative Grade (colloquially “below investment grade” or “junk”) — indicating elevated default risk.

Short-Term Credit Rating Grades in Bangladesh

For obligations with maturities of one year or less, a separate short-term rating scale applies:

| Grade | Interpretation |

|---|---|

| ST-1 | Superior capacity for timely repayment |

| ST-2 | Strong capacity for timely repayment |

| ST-3 | Satisfactory capacity; susceptible to adverse conditions |

| ST-4 | Moderate capacity; highly susceptible to adverse conditions |

| ST-5 | Weak capacity; uncertain timely repayment |

| ST-6 | Default or near default on short-term obligations |

Rating Modifiers: The Plus and Minus System

Within each major long-term rating category (AA through B), agencies apply “+” (plus) and “-” (minus) modifiers to indicate relative standing within the category. For example:

- AA+ indicates the higher end of the AA category — closer to AAA quality

- AA- indicates the lower end of the AA category — closer to A quality

This modifier system provides finer-grained differentiation than the primary letter grades alone, enabling more precise risk pricing by lenders and investors.

Rating Outlook and Watch Status

Beyond the grade itself, rating agencies communicate forward-looking signals through:

- Stable Outlook — The rating is unlikely to change in the medium term (12–24 months)

- Positive Outlook — The rating may be upgraded in the medium term

- Negative Outlook — The rating may be downgraded in the medium term

- Rating Watch (Positive) — An upgrade is under active consideration; typically triggered by a material positive event

- Rating Watch (Negative) — A downgrade is under active consideration; typically triggered by a material adverse development

- Rating Suspended — The agency has temporarily suspended the rating due to insufficient information

- Rating Withdrawn — The rating has been formally discontinued

The Credit Rating Process in Bangladesh: How Ratings Are Assigned

Stage-by-Stage Rating Methodology

The credit rating system in Bangladesh follows a structured analytical process that combines quantitative financial analysis with qualitative judgment:

Stage 1: Engagement and Mandate The entity (issuer or borrower) formally engages the rating agency. A mandate letter is executed confirming the scope, fee structure, and type of rating required (entity-level, instrument-level, or both).

Stage 2: Information Collection The rating agency issues a formal information request covering:

- Audited financial statements (minimum 3–5 years)

- Management accounts and financial projections

- Organizational structure and ownership details

- Industry and competitive position data

- Regulatory compliance status

- Existing debt structure and covenants

Stage 3: Management Meeting Senior rating analysts conduct a structured management interview with the entity’s CFO, CEO, and relevant operational heads. This session assesses management quality, strategic clarity, risk management practices, and governance standards — qualitative factors not fully captured in financial statements.

Stage 4: Financial Analysis Quantitative analysis examines:

- Profitability metrics — Net interest margin, EBITDA margin, return on equity, return on assets

- Leverage ratios — Debt-to-equity, net debt-to-EBITDA, debt service coverage ratio (DSCR)

- Liquidity analysis — Current ratio, quick ratio, cash conversion cycle

- Asset quality (for banks) — Non-performing loan (NPL) ratio, provision coverage, classified loan trends

- Cash flow analysis — Operating cash flow adequacy, capital expenditure requirements, free cash flow

Stage 5: Industry and Macro Analysis The entity’s financial profile is contextualized within its industry operating environment:

- Sector growth trajectory and cyclicality

- Competitive intensity and market position

- Regulatory environment and compliance risk

- Macroeconomic sensitivity — exchange rate, inflation, interest rate exposure

Stage 6: Rating Committee Review The lead analyst presents findings to an independent Rating Committee — a panel of senior analysts not involved in the primary analysis. The committee challenges assumptions, stress-tests projections, and arrives at a consensus rating grade through deliberative review. This committee structure is the primary institutional safeguard against individual analyst bias.

Stage 7: Notification and Appeal The assigned rating is communicated to the entity before publication. The entity has the right to present additional information or factual corrections within a defined response window. Rating agencies do not alter ratings based on commercial pressure — only new material information can trigger a pre-publication reassessment.

Stage 8: Publication and Surveillance The final credit rating report in Bangladesh is published and distributed. Annual surveillance reviews maintain the rating’s currency, with interim reviews triggered by material events such as significant acquisitions, sudden financial deterioration, or major regulatory actions.

Bank Credit Rating in Bangladesh: A Specialized Framework

Why Bank Ratings Operate Differently

Bank credit rating in Bangladesh involves additional analytical dimensions not present in corporate ratings, reflecting the unique risk profile of financial intermediaries:

- Asset quality assessment — Analysis of the classified loan portfolio, NPL trends, and provision adequacy is central to bank ratings in a market where NPL ratios have been persistently elevated

- Capital adequacy — Basel III compliance, Common Equity Tier 1 (CET1) ratios, and total capital adequacy ratios are evaluated against regulatory minimums and peer benchmarks

- Funding stability — Deposit concentration, wholesale funding dependence, and liquidity coverage ratios

- Systemic importance — Government ownership, implicit state support assumptions, and too-big-to-fail considerations influence ratings for state-owned banks

- Governance quality — Board independence, management depth, and internal audit effectiveness carry elevated weight in bank ratings given the sector’s governance challenges

Mandatory Rating Requirements for Banks

Bangladesh Bank has issued circulars requiring banks and non-bank financial institutions (NBFIs) to obtain credit ratings for:

- Subordinated debt issuances — All bank-issued subordinated bonds require a published credit rating

- Capital market instruments — Any bank-sponsored financial instrument listed on the DSE or CSE

- Interbank lending classification — Unrated banks may face restrictions or higher risk weights in interbank market participation

Mandatory Rating Requirements: When Is a Credit Rating Compulsory?

The credit rating system in Bangladesh includes several regulatory contexts where obtaining a rating is not optional:

- Listed company bond issuances — All corporate bonds listed on DSE or CSE require a valid credit rating published by a BSEC-licensed agency

- Asset-backed securities and sukuk — Structured finance instruments require instrument-level ratings

- Mutual fund credit assessments — Fixed-income mutual funds may require portfolio-level credit quality disclosures

- IPO-related debt instruments — Where an IPO involves debenture issuance, a credit rating is mandated

- Bank regulatory reporting — Bangladesh Bank’s risk-based capital framework assigns risk weights to counterparty exposures partly based on external credit ratings

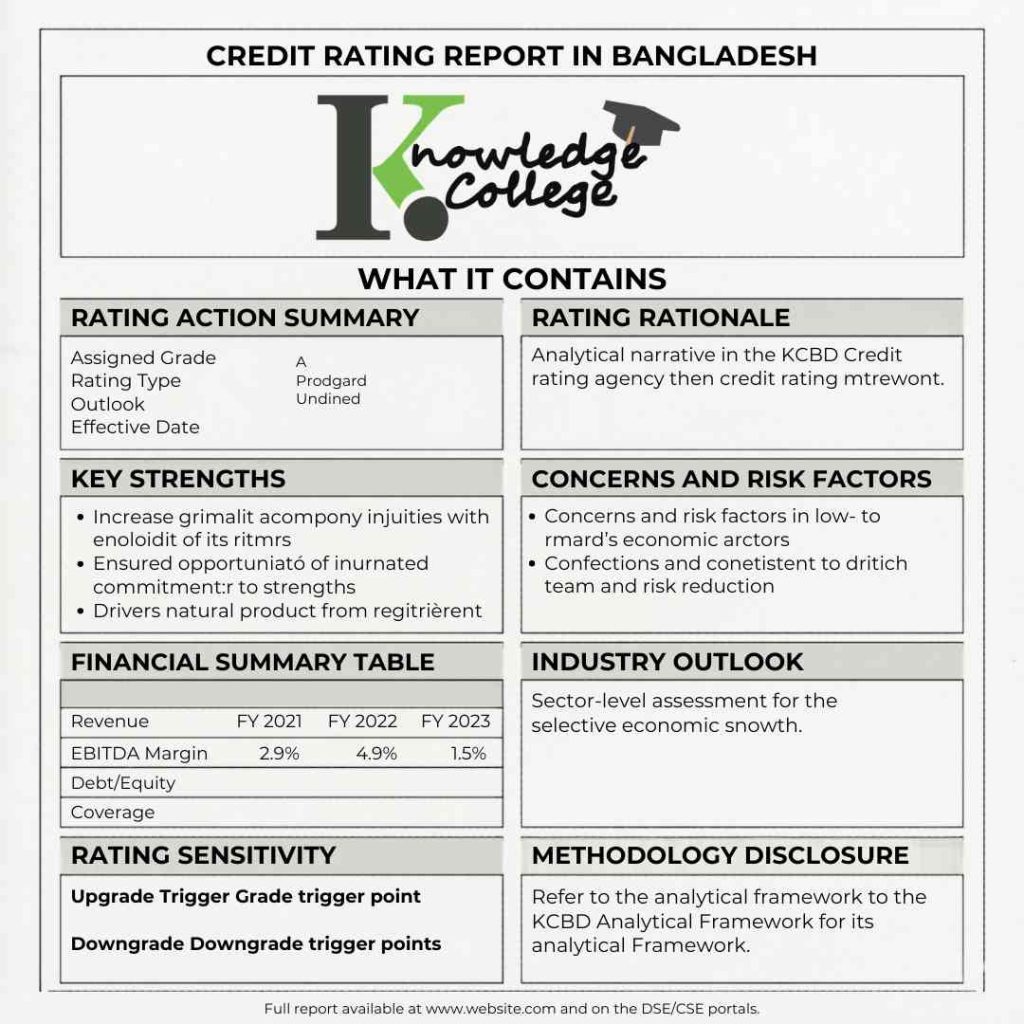

The Credit Rating Report in Bangladesh: What It Contains

A formally published credit rating report in Bangladesh is a structured analytical document. Its standard sections include:

- Rating Action Summary — The assigned grade, rating type (entity/instrument), outlook, and effective date

- Rating Rationale — A narrative explanation of the key factors supporting the assigned grade

- Strengths — Factors that positively support creditworthiness

- Concerns and Risk Factors — Elements that constrain the rating or represent downside risks

- Financial Summary Table — Key financial ratios over a 3–5 year historical period

- Industry Outlook — Sector-level assessment of the operating environment

- Rating Sensitivity — Explicit disclosure of what developments would trigger an upgrade or downgrade

- Methodology Disclosure — Reference to the analytical framework applied

Reports are typically published on the rating agency’s website and, for capital market-related ratings, on the DSE and CSE issuer disclosure portals. Investors and lenders can access these reports to inform their own credit analysis independently.

Expert Insight: The Structural Gaps in Bangladesh's Credit Rating Ecosystem

Bangladesh's credit rating industry has made measurable institutional progress since the Credit Rating Companies Rules of 1996. However, several structural gaps constrain its full effectiveness as a market discipline mechanism. First, the issuer-pays model — in which the rated entity compensates the rating agency — creates an inherent conflict of interest that requires robust methodological safeguards and genuine regulatory oversight to manage. Second, rating shopping — where issuers approach multiple agencies and select the most favorable outcome — remains a documented concern in the Bangladesh market. Third, the relatively small number of voluntary corporate ratings compared to the total population of significant private sector borrowers means credit rating's disciplinary function is applied to only a fraction of the entities that would benefit from it. Expanding mandatory rating requirements — particularly for large private borrowers accessing bank credit above defined thresholds — would materially strengthen the credit information ecosystem.

— Analytical perspective consistent with IMF Financial System Stability Assessment frameworks and ADB technical assistance reports on credit market development in South Asian frontier economies. Tweet

Common Myths About Credit Rating in Bangladesh

Myth 1: "A credit rating is only relevant for large corporations"

Reality: While Bangladesh’s current mandatory rating framework is most extensively applied to capital market issuers and banks, credit ratings benefit any entity that borrows, issues debt, or seeks third-party validation of financial credibility. Mid-sized companies that voluntarily obtain ratings consistently report improved negotiating leverage with lenders, lower interest rate margins, and faster credit approval timelines.

Myth 2: "A high credit rating guarantees no default will occur"

Reality: A credit rating is a probabilistic risk opinion — not a guarantee. An AAA-rated entity has an extremely low but non-zero default probability. Rating agencies explicitly state that ratings are opinions, not warranties. The 2008 global financial crisis, during which AAA-rated structured products defaulted catastrophically, is the most cited evidence that ratings can be wrong — particularly when underlying data quality or analytical assumptions are compromised.

Myth 3: "Once assigned, a credit rating doesn't change"

Reality: Credit ratings are dynamic assessments subject to continuous surveillance. A rating assigned today can be placed on Watch Negative tomorrow if material adverse information emerges — a major fraud discovery, sudden covenant breach, significant management departure, or macroeconomic shock. Annual review cycles ensure ratings reflect current financial conditions, not historical snapshots.

Myth 4: "Credit rating agencies in Bangladesh work for the companies they rate"

Reality: While the issuer-pays model means rated entities fund the rating process, rating agencies are legally and ethically obligated to maintain analytical independence. BSEC’s Credit Rating Companies Rules contain conflict-of-interest provisions, and agencies that systematically inflate ratings to retain clients face regulatory sanction and reputational destruction. Independence is the core commercial asset of any rating agency — without it, the ratings carry no market credibility and the agency’s business model collapses.

Myth 5: "My bank's credit score from CIB is the same as a formal credit rating"

Reality: These are fundamentally different systems. The CIB credit score from Bangladesh Bank is a data aggregation of past borrowing behavior — loans outstanding, repayment history, classified status. A formal credit rating from a BSEC-licensed agency is a forward-looking analytical opinion incorporating financial statements, management quality, industry dynamics, and macroeconomic context. One describes historical behavior; the other assesses future repayment capacity.

💡 Pro-Tip: How to Use Credit Ratings Strategically

For business borrowers: Obtain a voluntary credit rating before approaching lenders for significant facilities. A published rating from a BSEC-licensed agency signals transparency and analytical openness — qualities that materially improve lender confidence and can compress the credit negotiation timeline. Engage your rating agency annually, not only when a financing need arises; a track record of stable or improving ratings builds durable creditor relationships.

For investors: Always verify the current credit rating and outlook of any bond or debenture before investing. A BBB- rating with a Negative Outlook is a fundamentally different risk proposition than a BBB- rating with a Stable Outlook — despite carrying the same letter grade. Consult the full credit rating report in Bangladesh rather than relying solely on the summary grade.

Why Credit Rating in Bangladesh Matters for Economic Development

The systemic importance of a functioning credit rating system in Bangladesh extends well beyond individual transactions:

- Interest rate efficiency — Accurate risk pricing means low-risk borrowers pay appropriately lower rates; capital is allocated more efficiently across the economy

- Capital market deepening — Rated corporate bonds attract a broader investor base than unrated instruments, expanding the fixed-income market

- Bank NPL reduction — Lenders who incorporate external ratings into credit decisions benefit from an additional independent risk filter, complementing internal credit analysis

- Financial inclusion — As rating methodologies extend to SMEs and non-bank entities, previously opaque borrowers become more legible to formal financial institutions

- Foreign investment attraction — International institutional investors require rated instruments; a robust domestic rating ecosystem is a prerequisite for accessing global capital flows

Conclusion: Credit Rating in Bangladesh as a Financial Literacy Imperative

Understanding credit rating in Bangladesh is no longer a specialist competency reserved for investment bankers and credit analysts. It is a foundational element of financial literacy for anyone who borrows, invests, lends, or manages organizational finances in Bangladesh’s increasingly sophisticated capital market.

For beginners, the key insight is that credit ratings are risk opinions — standardized, independent assessments that reduce the information disadvantage faced by non-specialist investors and lenders. Understanding the difference between investment-grade and speculative-grade credit rating grades in Bangladesh is the single most actionable piece of knowledge for evaluating any debt instrument.

For C-suite executives, the credit rating is a strategic asset — one that must be actively managed, not passively accepted. The quality of financial disclosures, the consistency of debt service, and the transparency of governance practices all feed directly into the rating outcome. Organizations that treat the rating process as a routine compliance exercise consistently underperform those that engage with it as a strategic communication tool.

For hobbyists and financial analysts, the credit rating ecosystem — agencies, methodologies, scale architectures, regulatory mandates — provides an analytical framework for evaluating the entire fixed-income landscape of the Bangladesh capital market, from sovereign and bank paper to corporate debentures and structured instruments.

Credit rating in Bangladesh is the language in which financial risk is formally spoken. Fluency in that language is not optional for any serious participant in Bangladesh’s financial future.

📌 Quick Reference: Credit Rating in Bangladesh

- Primary Regulator: Bangladesh Securities and Exchange Commission (BSEC)

- Governing Rules: Credit Rating Companies Rules, 1996

- Licensed Agencies: CRAB, CRISL, ECRL, NCR, WASO, Alpha Credit Rating

- Long-Term Scale: AAA → AA → A → BBB → BB → B → CCC → CC → C → D

- Short-Term Scale: ST-1 through ST-6

- Investment Grade Threshold: BBB- and above

- Individual Credit Data: CIB (Credit Information Bureau), Bangladesh Bank

- Mandatory Contexts: Listed bonds, subordinated bank debt, structured instruments

- Rating Report Access: Rating agency websites; DSE/CSE issuer disclosure portals

This article is intended for informational and educational purposes only. It does not constitute financial advice, investment recommendations, or legal guidance. For specific credit rating requirements, consult a BSEC-licensed credit rating agency or a qualified financial professional.