Central Depository Bangladesh Limited (CDBL)

by Admin-KCBD · Published · Updated

The Paper Certificate Crisis No One Talks About

Imagine purchasing shares in a listed Bangladeshi company in 1995. The transaction is complete — but what you receive is not instant digital confirmation. It is a physical paper certificate: a document that can be lost in transit, forged by bad actors, damaged in a flood, or disputed in court for years. To transfer those shares to another buyer, you must physically hand over the certificate, wait for manual verification, and pray that the registrar processes the transfer without administrative delay or error.

This was the reality of the Bangladesh Stock Market before electronic custody existed. Share settlement took weeks. Disputes were endemic. Fraud was structurally enabled. Investors in both the DSE and CSE operated in an environment where the mechanics of ownership were as precarious as the investment itself.

The establishment of Central Depository Bangladesh Limited (CDBL) resolved this systemic vulnerability. It replaced physical certificates with electronic records, compressed settlement timelines from weeks to days, and created a secure, centralized register of beneficial ownership that underpins every securities transaction in Bangladesh’s capital market today.

This guide examines CDBL in complete depth — its full meaning, operational architecture, BO account system, role in the Bangladesh capital market, and why every investor must understand it before placing a single taka in the stock market.

What Is Central Depository Bangladesh Limited (CDBL)?

Central Depository Bangladesh Limited (CDBL) is the sole central securities depository of Bangladesh, responsible for the electronic custody, transfer, and settlement of all dematerialized securities traded on the Dhaka Stock Exchange (DSE) and the Chittagong Stock Exchange (CSE).

Incorporated as a public limited company under the Companies Act 1994, CDBL operates under the regulatory oversight of the Bangladesh Securities and Exchange Commission (BSEC) and was established under the Depositories Act, 1999.

In operational terms, CDBL performs the following core functions:

- Dematerialization — Converting physical share certificates into electronic book entries

- Custody — Maintaining the electronic register of all beneficial ownership positions

- Settlement — Processing the transfer of securities between buyer and seller accounts upon trade execution

- Corporate action processing — Crediting dividends, bonus shares, rights entitlements, and stock splits to investor accounts automatically

- Pledge and lien management — Recording securities pledged as collateral for margin financing or bank loans

CDBL is the invisible backbone of the Bangladesh capital market. Every share purchase on the DSE or CSE, every IPO allotment, every dividend credit — all pass through CDBL’s infrastructure.

CDBL Full Meaning: Decoding the Institution

Breaking Down the Name

CDBL stands for Central Depository Bangladesh Limited. Each component carries specific institutional meaning:

- Central — Singular, national scope. Unlike broker-level custodians, CDBL is the apex registry — one centralized system that holds the master record of all securities ownership in Bangladesh

- Depository — The core function: safe custody and electronic maintenance of securities in dematerialized form, eliminating physical certificate risk

- Bangladesh — National jurisdiction. CDBL’s mandate covers all securities listed and traded within Bangladesh’s regulated capital market

- Limited — Corporate structure. CDBL is incorporated as a public limited company, giving it a defined shareholder base, board governance structure, and financial accountability framework

Ownership and Governance Structure

| Shareholder Category | Description |

|---|---|

| DSE (Dhaka Stock Exchange) | Major institutional shareholder |

| CSE (Chittagong Stock Exchange) | Institutional shareholder |

| Licensed Banks and Financial Institutions | Including state-owned and private commercial banks |

| Insurance Companies | Institutional shareholders |

| BSEC-Regulated Entities | Various capital market institutions |

CDBL’s board of directors includes representatives from its institutional shareholders alongside independent directors appointed in compliance with BSEC’s corporate governance directives. This ownership structure ensures that the depository’s governance is aligned with the interests of the broader capital market ecosystem rather than any single commercial interest.

Historical Context: Why Bangladesh Needed CDBL

The Pre-CDBL Capital Market Environment

Before Central Depository Bangladesh Limited became operational, Bangladesh’s securities settlement system was characterized by:

- Physical share certificates as the primary instrument of ownership proof

- Manual transfer processes requiring physical delivery of certificates between brokers and registrars

- Settlement periods of T+7 or longer — meaning a trade executed today would not be fully settled for a week or more

- Rampant certificate fraud — forged certificates were a documented systemic problem

- Lost and damaged certificates — creating ownership disputes that clogged civil courts

- High administrative costs associated with physical certificate management across the entire market chain

These frictions were not minor inconveniences. They represented fundamental barriers to market development, institutional investor participation, and investor confidence.

Establishment and Operational Launch

| Year | Milestone |

|---|---|

| 1999 | Depositories Act enacted; legal foundation for CDBL established |

| 2000 | Central Depository Bangladesh Limited incorporated as a public limited company |

| 2003 | CDBL commenced operations; first securities dematerialized |

| 2004 | Full integration with DSE trading and settlement systems |

| 2005 | CSE settlement integrated into CDBL infrastructure |

| 2006 | Online BO account statement access introduced |

| 2010+ | Continuous system upgrades; corporate action automation expanded |

| 2021+ | Digital BO account opening initiatives accelerated |

The transition from physical to electronic custody was not instantaneous. A phased dematerialization program progressively moved all listed securities into the CDBL system over several years, with mandatory dematerialization ultimately enforced for all new IPO allotments and listed security transfers.

The BO Account: CDBL's Central Investor Interface

What Is a BO Account?

A BO Account — formally, a Beneficiary Owner Account — is the electronic account maintained within CDBL’s system that records an individual investor’s holdings of dematerialized securities. Every person who wishes to invest in the Bangladesh Stock Market through the DSE or CSE must possess a valid, active BO account.

The BO account is the investor’s digital vault. Just as a bank account holds cash, the BO account holds securities — shares, mutual fund units, debentures, and other eligible instruments — in electronic form.

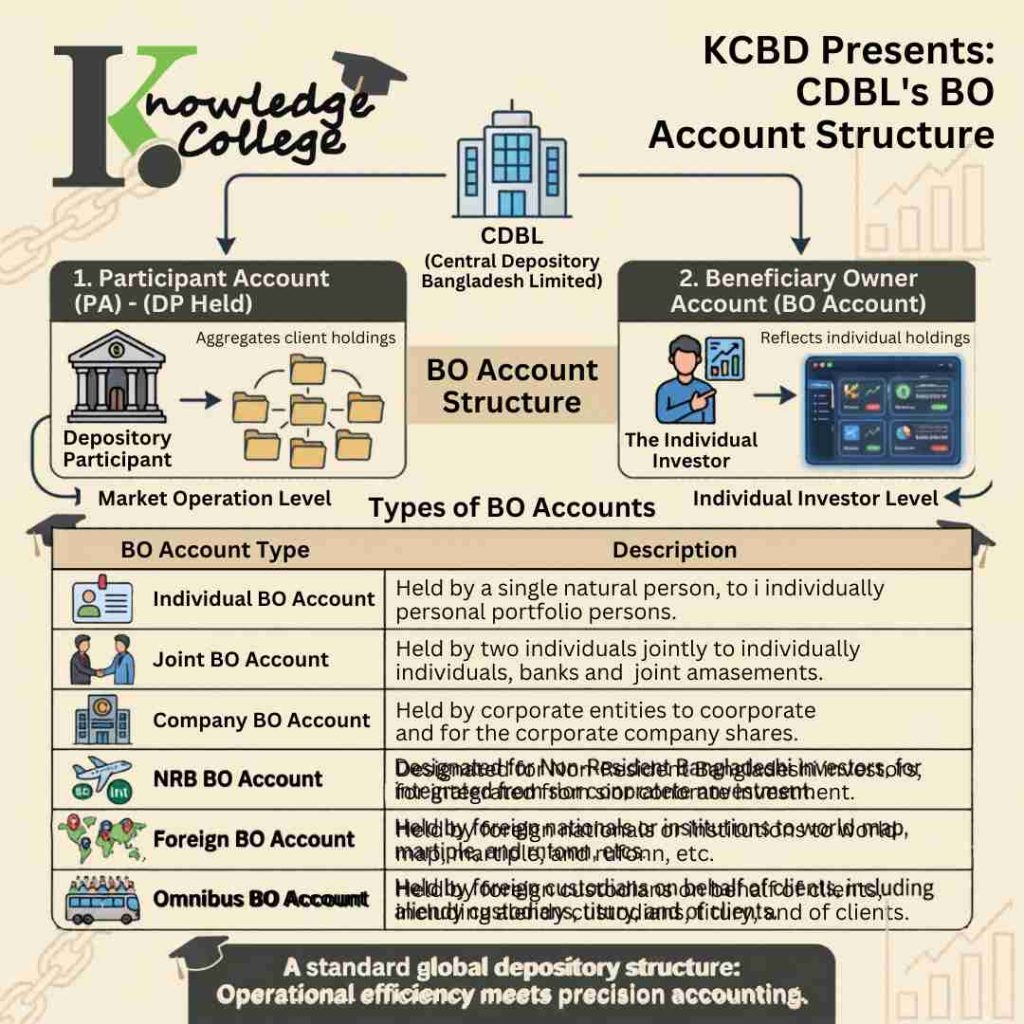

BO Account Structure

CDBL’s account architecture involves two distinct account levels:

1. Participant Account (PA) Held by CDBL-registered Depository Participants (DPs) — typically licensed stockbrokers or custodian banks. The Participant Account aggregates the holdings of all clients under that participant.

2. Beneficiary Owner Account (BO Account) The individual investor’s account, sub-ledgered under the relevant Participant Account. This is the account that reflects the investor’s specific security holdings and transaction history.

This two-tier structure is a global standard for central depository architecture, balancing operational efficiency at the participant level with individual investor-level accounting precision.

Types of BO Accounts

| BO Account Type | Description |

|---|---|

| Individual BO Account | Held by a single natural person; most common account type |

| Joint BO Account | Held by two individuals jointly; both signatories required for certain transactions |

| Company BO Account | Held by corporate entities — limited companies, partnerships, institutions |

| NRB BO Account | Specifically designated for Non-Resident Bangladeshi investors |

| Foreign BO Account | Held by foreign nationals or foreign institutional investors |

| Omnibus BO Account | Held by foreign custodians on behalf of multiple foreign clients |

How to Open a BO Account: Step-by-Step Process

Standard BO Account Opening Procedure

Opening a BO account is the mandatory first step for any investor seeking to participate in the Bangladesh capital market. The process is administered through Depository Participants (DPs) — CDBL-registered entities that serve as the interface between investors and the central depository.

Identify a CDBL-registered Depository Participant — These include DSE and CSE-licensed stockbrokers, commercial banks with DP licenses, and merchant banks. Verify DP status on the CDBL official portal (cdbl.com.bd)

Obtain and complete the BO Account Opening Form — Standard forms are provided by the DP; they require comprehensive personal and financial information

Compile required documentation:

- Valid National Identity Card (NID) — mandatory

- Tax Identification Number (TIN) — mandatory for all account types

- Two recent passport-size photographs

- Bank account details (cancelled cheque or bank statement)

- For joint accounts: documentation for both account holders

- For corporate accounts: Certificate of Incorporation, Memorandum and Articles of Association, board resolution

Submit the completed application to the DP — Along with all supporting documents for KYC (Know Your Customer) verification

DP verification and CDBL registration — The DP reviews the application, performs KYC due diligence, and submits the account creation request to CDBL

Receive BO Account Number — A unique 16-digit BO account number is issued upon successful registration

Activate the account — Fund the linked trading account and the BO account is ready for securities transactions

Online BO Account Opening

BSEC and CDBL have progressively expanded online BO account opening capabilities to reduce friction and extend market access:

- Designated DP portals — Many stockbrokers and banks offer digital application submission through their websites or mobile applications

- e-KYC capabilities — Electronic identity verification using NID database integration reduces physical document submission requirements

- Digital signature provisions — Regulatory approvals for digitally executed BO account agreements

- NRB-specific online pathways — Bangladeshi diaspora investors can initiate BO account opening from abroad through designated online channels

💡 Pro-Tip — Online BO Account Verification: Before submitting any online BO account application, verify the Depository Participant’s registration status directly on cdbl.com.bd. Fraudulent entities impersonating legitimate DPs have targeted retail investors through unofficial websites and social media channels. CDBL’s official DP registry is the single authoritative verification source. No legitimate DP will request payment for BO account opening through unofficial payment channels.

How CDBL Works: The Settlement Cycle Explained

Trade-to-Settlement Flow

Every securities transaction on the DSE or CSE follows a defined settlement pathway that passes through CDBL’s infrastructure:

Trade Execution (T) — Buyer and seller orders match on the exchange’s electronic trading platform; trade confirmed in the exchange system

Trade Data Transmission (T) — Exchange transmits matched trade data to CDBL in real time

Obligation Calculation (T+1) — CDBL calculates net settlement obligations for each Depository Participant — the aggregate securities to be delivered and received

Securities Settlement (T+2) — On the second business day after trade execution, CDBL transfers securities from the seller’s BO account to the buyer’s BO account through book entry — no physical movement occurs

Funds Settlement (T+2) — Simultaneously, the corresponding cash settlement flows through the exchange’s designated settlement bank

Confirmation — Both buyer and seller DP accounts are updated; the transaction is irrevocably complete

The T+2 settlement cycle — two business days from trade to settlement — is the current Bangladesh standard, aligned with international settlement norms and a significant operational improvement from the pre-CDBL era of T+7 or longer.

Corporate Action Processing

CDBL automates the distribution of corporate benefits to all eligible BO account holders:

- Cash dividends — Credited directly to the investor’s bank account linked to the BO account, eliminating paper dividend warrants

- Stock dividends (bonus shares) — Credited to the BO account on the record date

- Rights entitlements — Rights shares are credited to eligible BO accounts; investors can subscribe or renounce through the DP

- Stock splits and consolidations — Adjusted automatically in CDBL’s system with no investor action required

- IPO allotments — Allotted shares are credited directly to applicants’ BO accounts upon IPO finalization

CDBL's Role in the Bangladesh Capital Market Ecosystem

Integration With DSE and CSE

Central Depository Bangladesh Limited operates as the settlement counterparty for both major exchanges:

- All DSE-executed trades settle through CDBL’s book-entry system

- All CSE-executed trades settle through the same CDBL infrastructure

- This unified settlement layer means a security can be traded on either exchange with settlement processed through a single centralized system — eliminating inter-exchange settlement complexity

The Dematerialization Mandate

CDBL enforces and administers the mandatory dematerialization of all securities listed on the DSE and CSE. Key provisions include:

- New IPO allotments are issued exclusively in electronic form directly to CDBL BO accounts — no physical certificates for new issues

- Existing physical certificates must be dematerialized through a formal conversion process before trading

- Transfers of listed securities cannot be effected in physical form — all changes of ownership require electronic settlement through CDBL

Pledge and Hypothecation Services

CDBL enables securities-backed lending by maintaining formal records of pledged holdings:

- Investors can instruct CDBL (through their DP) to mark specific shareholdings as pledged collateral in favor of a lender — typically a bank or margin financing broker

- The pledge is recorded in CDBL’s system, preventing the pledged securities from being transferred or sold without the lender’s consent

- Upon loan repayment, the pledge is released and the securities revert to the investor’s free custody balance

This service enables investors to access margin financing and securities-backed loans within a legally structured, centrally recorded framework — reducing the risk of collateral disputes.

Expert Insight: CDBL's Systemic Importance in Frontier Market Development

Central securities depositories are not ancillary infrastructure — they are the foundational trust layer of any functional capital market. Without a reliable, centralized, electronic custody system, institutional investors cannot participate, settlement risk remains unacceptably high, and market liquidity is structurally constrained. CDBL's establishment and evolution represents one of Bangladesh's most consequential capital market reforms. The transition from physical certificate settlement to T+2 electronic settlement fundamentally altered the risk profile of market participation — and that change, more than any single regulatory intervention, enabled the institutional investor base to begin developing. The next frontier is real-time settlement and further integration with cross-border custody frameworks.

— Analytical perspective consistent with World Bank Financial Sector Development reports and Asian Development Bank (ADB) capital market infrastructure assessments for South and Southeast Asian frontier markets. Tweet

Common Myths About CDBL

Myth 1: "CDBL holds my money, not my shares"

Reality: CDBL holds your securities — not cash. Your shares, mutual fund units, and other dematerialized instruments are recorded in your BO account. Cash for purchasing securities is held in a separate trading account maintained by your broker or bank. The two accounts serve distinct functions and are governed by separate regulatory frameworks.

Myth 2: "If my broker closes down, I lose my shares"

Reality: This is one of CDBL’s most critical investor protection features. Your BO account is yours — not your broker’s. If a Depository Participant ceases operations, goes bankrupt, or loses its license, CDBL’s records of your holdings are fully preserved. You can transfer your BO account to another DP and continue uninterrupted access to your securities. Your holdings exist independently of your broker’s financial health.

Myth 3: "I need a separate BO account for DSE and CSE"

Reality: A single BO account covers securities traded on both the DSE and the CSE. There is no requirement for exchange-specific accounts. One BO account, one DP relationship, and one portfolio register covers your entire Bangladesh capital market position.

Myth 4: "Opening a BO account requires visiting Dhaka"

Reality: BO accounts can be opened through any CDBL-registered Depository Participant nationwide — including bank branches and brokerage offices located in Chittagong, Sylhet, Rajshahi, Khulna, and other cities. Online BO account opening options further eliminate geographic barriers, enabling investors across Bangladesh and abroad to initiate the process digitally.

Myth 5: "CDBL is only relevant during share purchases"

Reality: CDBL is active throughout the entire lifecycle of an investment. It processes IPO allotments, records share purchases, settles sales, distributes cash dividends, credits bonus shares, manages rights entitlements, and records collateral pledges. Every material event in an investor’s portfolio passes through CDBL’s system — it is not a one-time transaction facility but a continuous custody and servicing infrastructure.

Risks, Responsibilities, and Investor Best Practices

Every BO account holder carries specific responsibilities that directly affect the security and accuracy of their holdings:

- Keep KYC information current — Changes in address, NID, bank account, or contact information must be reported to the DP promptly; outdated KYC can prevent corporate action proceeds from reaching the investor

- Verify BO account statements regularly — Monthly review of CDBL statements detects unauthorized transactions, missing corporate action credits, or data discrepancies at the earliest opportunity

- Guard BO account credentials — Online portal access credentials must be protected with the same rigor as banking passwords; unauthorized access to BO account details creates transfer fraud risk

- Nominate a nominee — Designating a nominee in the BO account documentation ensures that holdings can be claimed by dependents in the event of the investor’s death without protracted legal proceedings

- Monitor DP license status — Periodically verify that your DP remains in good regulatory standing on the CDBL and BSEC official registries

Conclusion: Central Depository Bangladesh Limited as the Trust Foundation of Every Investment

No share purchase on the DSE, no IPO application on the CSE, no mutual fund unit in any Bangladeshi collective investment scheme exists in the formal capital market without passing through Central Depository Bangladesh Limited (CDBL). It is not a peripheral administrative function — it is the structural trust layer upon which the entire Bangladesh capital market rests.

For beginners, understanding CDBL means understanding that your securities are held securely, independently of your broker’s financial health, in a centralized electronic system with unambiguous records of ownership. Opening an online BO account through a CDBL-registered Depository Participant is the non-negotiable first step on the investor journey.

For C-suite executives, CDBL’s infrastructure is directly relevant to IPO planning, securities-backed financing, corporate action administration, and investor relations. Every equity instrument your organization issues will be dematerialized and custodied through CDBL’s system — understanding that architecture is fundamental to capital market strategy.

For hobbyists and financial analysts, CDBL’s aggregate data — total BO accounts, dematerialized securities volume, settlement velocity — constitutes a rich dataset for assessing the depth, breadth, and health of the Bangladesh capital market over time.

The Bangladesh stock market is only as trustworthy as the infrastructure that records and safeguards ownership. Central Depository Bangladesh Limited (CDBL) is that infrastructure. Understanding it is not optional — it is foundational.

📌 CDBL Quick Reference

- Full Name: Central Depository Bangladesh Limited

- Established: 2000 (Depositories Act enacted 1999)

- Operations Commenced: 2003

- Headquarters: Dhaka, Bangladesh

- Regulator: Bangladesh Securities and Exchange Commission (BSEC)

- Governing Law: Depositories Act, 1999

- Exchanges Served: DSE (Dhaka Stock Exchange), CSE (Chittagong Stock Exchange)

- Settlement Cycle: T+2 (two business days post-trade)

- Account Type: Beneficiary Owner (BO) Account

- Official Website: cdbl.com.bd

This article is produced for informational and educational purposes only. It does not constitute investment advice or legal guidance. For account-specific queries, contact your CDBL-registered Depository Participant or visit cdbl.com.bd directly.